At no point in history have people thought more about what they eat, or eaten worse.

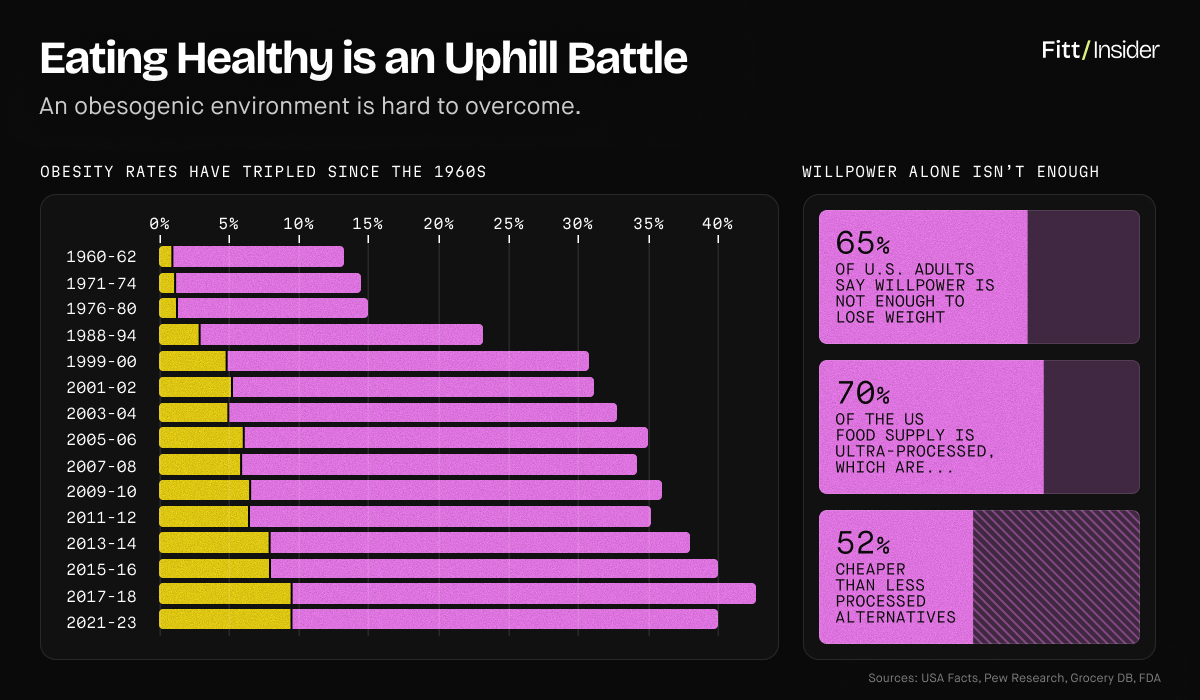

Today, ~40% of US adults are obese, 67% of kids’ calories are ultra-processed, and eating disorders are rising worldwide. Diet tribalism, political lobbying, and deceptive marketing have left eight in 10 consumers unsure who/what to trust.

But there’s a shift happening.

Spending on natural and organic products is up 545% since 2001, healthiness is the fastest-rising purchase factor, insurgent brands are outpacing legacy CPG, and GLP-1s are altering what—and how much—Americans eat. The data reflects a better food system being shaped in real time.

As shopping preferences align with health outcomes, reform can follow the same playbook as corruption: satisfy consumer cravings.

Pt. I: Acquired Tastes

The future of food starts with the brain.

Circa 2006, neurogastronomy showed flavor is constructed by the brain, not the tongue, with eating influenced by taste, smell, memory, and emotion. What’s more, stress and anxiety can cause insulin resistance and metabolic dysfunction, regardless of diet.

In other words, it’s not just what we eat, but how we feel when we eat that matters. Obsessively worrying about food is scientifically counterproductive.

Emerging R&D strategy, Givaudan partnered with neuroscience startup THIMUS, using its EEG x AI tech to decode tasters’ subconscious feelings for wellness-focused food science insights.

Fed Lies

Durable CPG brands serve culture, not just nutrition.

Corporate marketing has intuitively exploited neurogastronomy for ages. The original Coca-Cola was a medicinal tonic that never quite took off. Under new ownership, it reworked its formula and ads, loudly projecting national pride while quietly skimping on quality.

An early “clean” brand, Heinz became a staple by selling preservative-free ketchup in transparent glass bottles while advocating for industry-wide food safety regulations. It later swapped in corn syrup and flavoring but remained the subjective benchmark for “real” ketchup.

From breakfast cereal to potato chips, today’s iconic snacks were yesteryear’s cultural glue, and nostalgia keeps them sticky. But as wellness eats the world, the gap between these brands’ cultural stories and physical products has become too obvious to ignore.

Split Check

Wellness and inflation are redefining value on both ends.

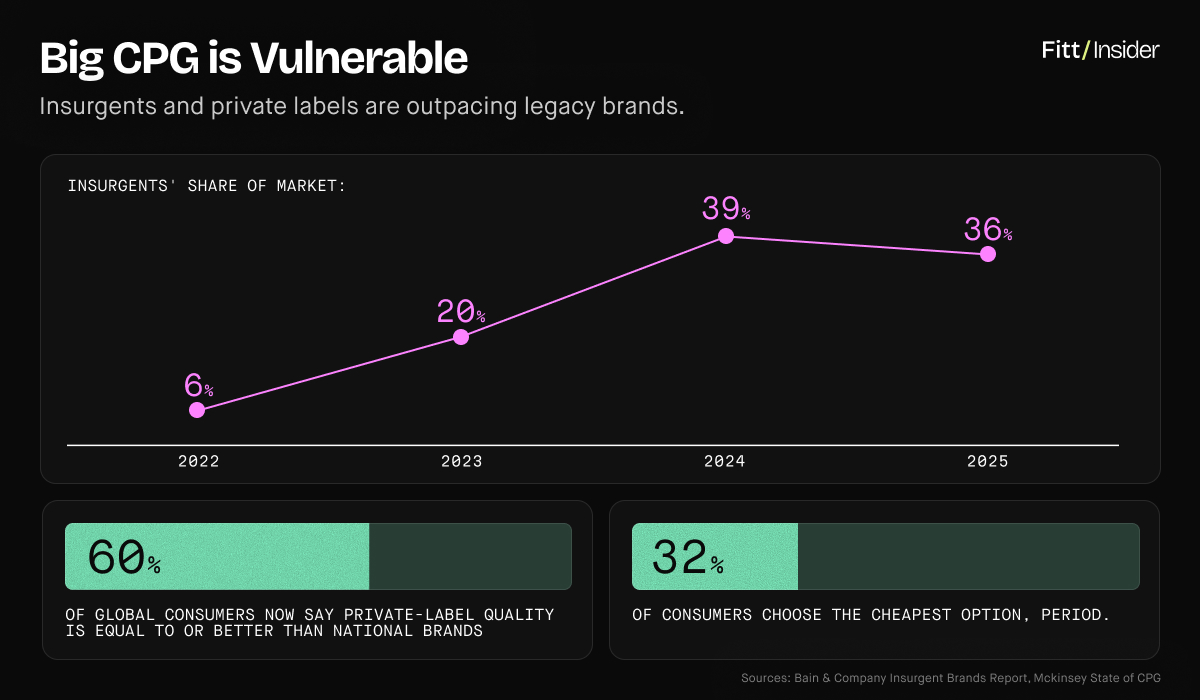

Spending data suggests Big Food is vulnerable. Straining households, food prices have spiked ~31% since 2019. In the K-shaped economy, the wealthiest consumers are buying trendy brands at luxe specialty grocers, as everyone else seeks the cheapest option that meets their needs. Yet, even among six-figure earners, 70% say they now shop at discount grocers for essentials, reserving splurges for special “little treat” products.

Unexpectedly, lower-income consumers are driving the fastest growth in natural product spend as private label unlocks access. Store brand sales have jumped 23% in four years, rising to >20% market share, and 80% of consumers say the quality now matches national brands.

The new product pipeline, when Once Upon A Farm debuts $3 organic baby food pouches, Nestlé is pressured to answer with a $2 Gerber version, then Target launches a $1 Good & Gather dupe. The trendy brand never trickles down, but copycats do.

Notably, high- and low-income shoppers are feeding different wellness motivations. The former pays a premium for identity x belonging. The latter is cleaning up toxic exposures on the cheap. Stuck in the middle, legacy brands increasingly satisfy neither, relying on M&A to stay relevant.

Broadly speaking, F&B CPG is underperforming, but premium/functional/healthy options are growing twice as fast as the overall category. Outliers, better-for-you insurgents gained ~55% YoY on volume. Predicting a permanent shift in consumer values, nearly half of CPG execs say their current business model won’t survive the decade.

Bitter Pill

The food industry is being reshaped by what consumers won’t eat.

Morgan Stanley conservatively projects 30% of the obese population will be on weight loss drugs by 2035 (vs. just 6% in 2025). EY-Parthenon estimates medication-induced diet changes will spark a $12B loss in 10-year snack sales, as GLP-1 users consume >20% fewer calories. With tastes being fundamentally reshaped, Nestlé, Danone, PepsiCo, and the like are diversifying portfolios around wellness.

Meanwhile, MAHA has mobilized a demographic academia never could. On alert, 25K Americans are downloading food scanning app Yuka daily, and 94% of users have put back low-scoring products. Doing their own research, consumers are driving change faster than policy, with conglomerates reportedly reformulating to boost their Yuka rating.

Still, ingredient moralization isn’t a long-term brand strategy. Better-for-you is the new baseline, not a differentiator. From Magic Spoon to Siete and OLIPOP, insurgents scaling on joy, authenticity, and nostalgia—not anxiety—are best positioned to become household names.

What it means: The opportunity isn’t vilifying “bad” foods but replacing conglomerates’ hold on core memories by revamping rituals. Storybrands create culture; dupes just extend access. Exacerbated by GLP-1s, the next generation’s comfort foods are being decided right now.

Pt II: The Long Table

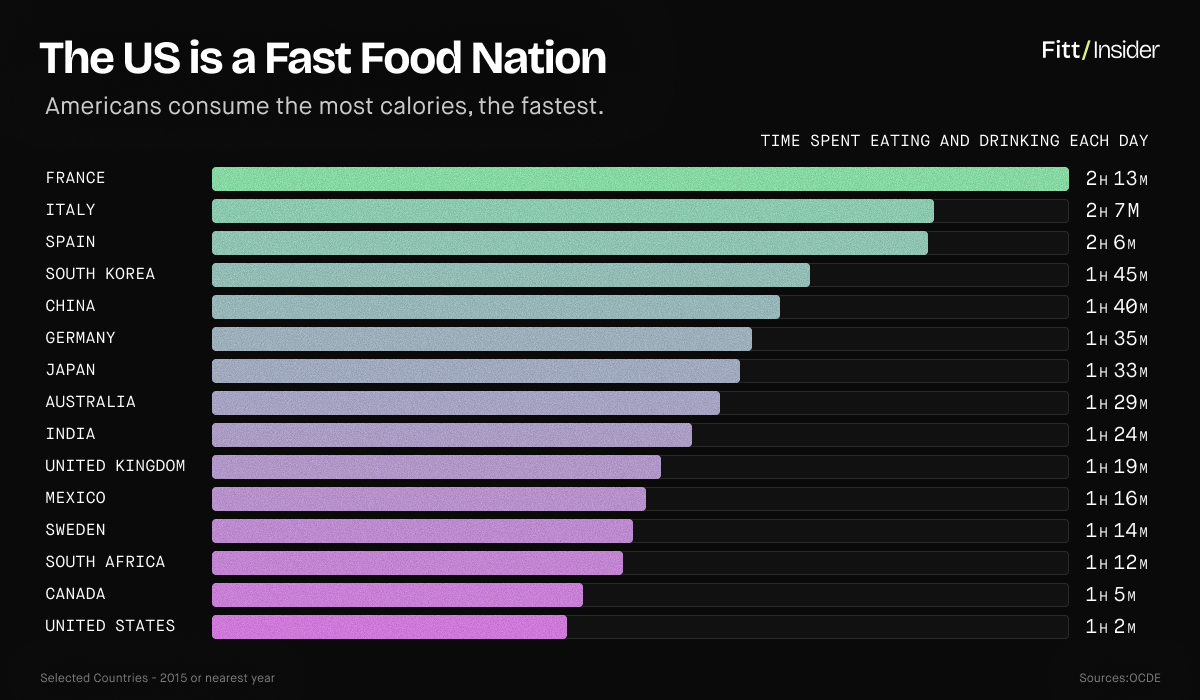

Hyperconvenience culture erased our OG wellness hack: the communal meal.

Not just a romantic ideal, the “long table” was health infrastructure. Children who eat three or more family meals a week are 35% less likely to develop disordered eating habits, 24% more likely to eat healthier foods, and 12% less likely to become obese, yet family dinner time has declined 30% in 30 years.

Even at school, time for savoring shared meals has shrunk. With most lunches lasting ~20 minutes, kids have <10 to scarf food after accounting for walking, lines, and bathroom breaks — despite studies showing kids eat healthier when given more time. Corporate culture is no better, with a third of Americans eating at their desks and 43% multitasking during lunch.

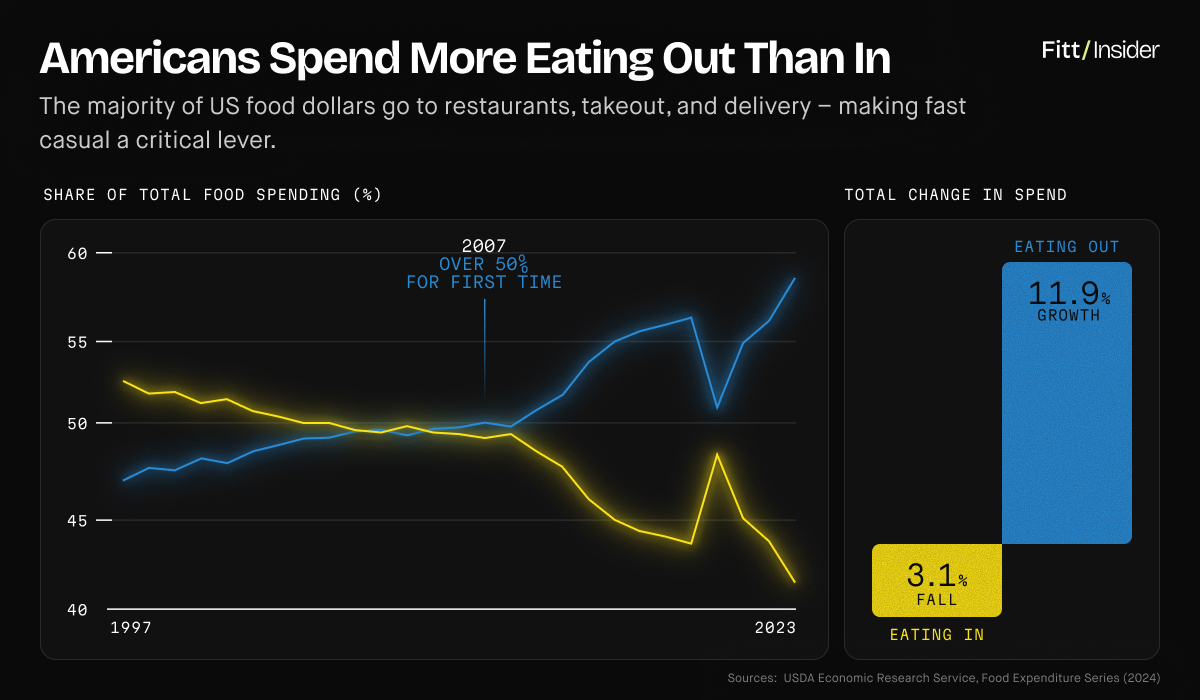

But the socioeconomic reality is many people lack time to cook. As prepared food eclipses homemade meals, fast-fine must meet the moment.

Eating Out

Middle-class restaurants need a makeover.

A pendulum shift, societal desire is shifting away from screens toward sensory experience x connection, with restaurant budgets peaking post-COVID. Meanwhile, credit card analysis shows GLP-1 users choosing experiential dining over fast food — indicating growing appreciation for intentional meals over pure convenience.

Assembly line “slop bowls” are losing appeal, exposing the limits of optimization as brand identity. Associated with biohackers and sad desk salads, Sweetgreen shares declined almost 80% in one year, same-store sales fell 11.5% in Q4 2025, traffic dropped 13.3%, and the company sold its robotics unit Spyce to Wonder for $186M.

Per Placer.ai, price-sensitive middle-income diners are pressuring quick-service and fast-casual concepts to upgrade in-store experience. More than tech companies masquerading as restaurants, people want healthy neighborhood anchors with creative, culturally relevant menus.

Next-gen fast-casual must find a middle ground, raising the bar on food quality while retaining purpose and belonging as equally important pillars of the experience.No restaurant serves all tastes, but local spots across the country are assembling the right ingredients:

Ggiata (LA) — Born from nostalgia for East Coast Italian delis, Ggiata’s six locations highlight local artists while serving as a “central meeting point” for friends and family.

Tacombi (NYC) — A full-stack cultural brand, the 22-location taqueria chain spawned CPG spinoff Vista Hermosa tortillas and a foundation that distributes food to nearby communities.

Skratch Labs Table (Boulder) — Redefining high performance, the endurance sport brand built a full-service restaurant on the belief active nutrition is about shared meals, not just macros.

Hilltop Coffee + Kitchen (LA) — Mixing quality ingredients with creative energy, the Issa Rae-backed cafes double as collab spaces for entrepreneurs in underserved neighborhoods.

ChòpnBlok (Houston) — A “cultural crossroads,” the West African fast-casual concept serves community programming alongside food from a James Beard Award-semifinalist chef.

People are hungry for meaning. Chains that embrace third space energy, experience design, menu transparency, ingredient sourcing as brand storytelling, and/or chef-driven credibility plays while positioning as cultural beacons can have outsized impact.

Eating In

Health, convenience, and affordability remain an elusive trifecta.

Home cooking correlates to better health outcomes, but busy schedules and tight budgets are barriers. Just 20% say their diet is “very healthy,” and despite expressing intent, people aren’t eating enough veggies. Theoretically on board, 75% would prefer using food over prescription drugs to manage health but require guidance, convenience, and affordability.

Fishwife’s breakout success showed consumer demand for nutritious, pre-flavored whole foods, and its Costco placement is helping democratize pricing. Replicating the formula with produce, Row 7 is tinning flavor-bred veggies for easy weeknight meals, and Fruitist raised $150M to make jumbo berries America’s favorite snack.

A pain point, 70% of adults are concerned about chemicals in food, but willingness to pay a “purpose tax” for sustainable/regenerative goods has dropped from 83% to 65% among $100K+ households since 2024. Helping justify higher spend, Edacious quantifies the increased nutrient density of organic regenerative goods — making the ROI personal, not just moral.

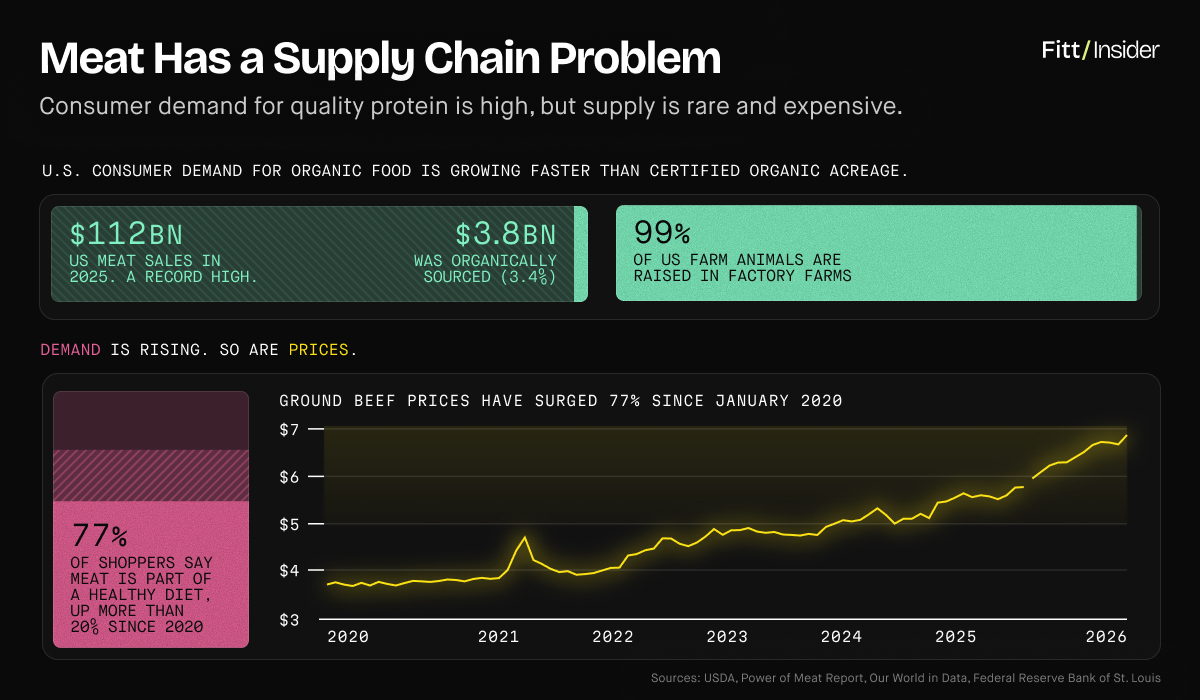

Meanwhile, meat is rising in both cost and volume sales, hitting a record-high $112B last year, but much of it is poor quality. With 99% of livestock animals factory farmed, 89% of regenerative shoppers struggle to find products in stores, fueling the rise of subscription services like Force of Nature and Seatopia.

Drone-to-Table

AI could put personalized nutrition on autopilot.

From Oura Meals to Alma and MyFitnessPal, nutrition tracking apps are getting smarter, reducing the friction of manual entry with AI photo logging and wearable integrations. While greater adherence has benefits, there’s danger in gamification fueling obsessiveness, discounting the immeasurable joy of dessert with friends or a heritage dish with bad macros.

Still, for GLP-1 users, precision takeout concepts like LA’s SUMMITS and NYC’s Matter could help recalibrate relationships with food. A crucial behavior change window, 67% say the drugs made it possible to rewire their brain. Per Noom, people who built healthy habits on the drugs were twice as likely to maintain weight loss, and 96% maintained habits after quitting meds.

Looking ahead, innovators see AI as a personalized nutrition cost balancer. From Travis Kalanick’s vision for an “internet food court” and private robo-chefs to Sweetgreen’s pivot toward “Spotify for food,” making healthy meal delivery a mass-market luxury is tech’s domain. If incentives align, automation could prove especially valuable for food-as-med patients.

All-in on AI, Marc Lore is building a national food OS with Wonder. Users will set spending and biometric targets based on blood and body comp tests, then receive tailored meals. Aiming to erase food deserts, the company will cut labor costs with robotics, using savings to lower prices rather than boost margins. Lore’s goal is 10K “programmable kitchen” locations by 2040, reaching 90% of the population with 20% lower prices and 20-minute drone delivery.

What it means: The healthiest relationships with food leave room for both precision and pleasure. The key for brands is knowing which diet periodization phase their core customer is in.

Pt III: Institutional Menus

Consumers are pulling the market, but infrastructure must follow.

Clinical food-as-medicine programs could assist the most vulnerable while saving $1T+ annually in diet-related disease costs. Scaling up, startups like Foodsmart, Fay, and Berry Street are expanding access to in-network dietitians. Making progress measurable, Nourish and Noom integrated labs into their coaching platforms.

Schools are prime places for intervention, but 99% of school nutrition directors say they need more funding to improve menus, with many limited to microwaves and volunteer staff. Trying to bridge gaps, JOYN Foods’ 50Cut mushroom meat extenders earned approval in South Carolina K–12s, and Everytable is serving scratch food across Compton Unified.

Rethinking food processing itself, Harvard scientists developed Lasso, a centrifuge-based machine that weaves protein and fiber together without artificial binders, gums, or additives. Tackling chemical controversy, alternative ag strategies like Saga Robotics’ use of UVC light and Azaneo’s electro-weeding approach are being tested.

Financing a sustainable future, Mad Capital deployed $78M to help farmers survive the 36-month transition to organic methods, and the USDA announced a $700M regen ag pilot — while McDonald’s dedicated $200M and PepsiCo, Unilever, and others vocally co-committed. With hazy definitions of regenerative, skeptics warn of greenwashing, but it’s something.

What it means: Consumers can reshape markets, yet upstream fixes—from glyphosate use and soil quality to school lunches—require deep tech and institutional investment. America’s sad defaults are rooted in flawed incentives, not failures of willpower.

Food for Thought

Every era produces a version of the same argument: eat this, not that. Fear the fat, cut the carbs, avoid the seed oils. The specifics change, but the underlying logic—that food is a problem to be solved through discipline—doesn’t. And it keeps not working. Cultures with the healthiest relationships to food aren’t the most informed; they’re the most embedded.

Hyperpersonalized nutrition is valuable, especially to support those establishing healthier habits, but it overlooks food’s societal role. Cooking conveys care. Breaking bread bonds people. Cuisines carry memory and meaning across generations in ways no protocol ever will. Food companies and services must help consumers balance pleasure with personal health.

Reason for hope, Big Food’s cultural chokehold is loosening, with many of today’s kids’ tastebuds being shaped by insurgents. As progressive brands scale and consumer transparency tools like wearables, routine bloodwork, AI nutrition scanners mature — gaps between what’s on labels and what’s in products will only get harder to hide.

To move forward, the future of food must take cues from the past.

Beyond ingredients, brands should be redesigning how we gather and engage with food in daily life. UPFs spread by becoming cornerstones of culture, and their inverse must do the same. A big win, better-for-you is becoming the default, but trust, taste, and cultural acuity will become the new differentiators.